When someone writes an IOU, they are basically saying, ‘I owe you or your company something of value.’ A promise to pay letter or promissory note is built on the same idea but is more detailed and thorough. It identifies the dollar amount owed by the borrower, the interest rate, the names of the lender and borrower, and the payment timeline, among other details. This article reviews this crucial document, how to prepare it, and what it means for you or your business.

What Is a Promise to Pay Letter?

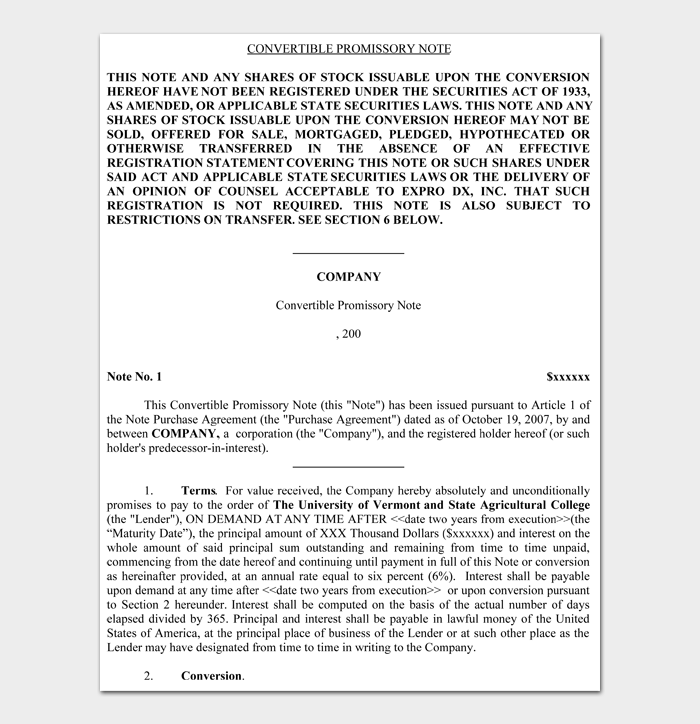

A promise to pay letter is also called a promissory note and is a DIY contract that promises payment to a given individual or entity by a set timeline. You can think of it as a more comprehensive and legally binding IOU. Generally, it is used by a private bank or investor to hold a borrower accountable for repaying a loan they have received. It also comes in handy when filing taxes.

The Process of (Promissory Note) Promise to Pay Letter

While a promissory note is a legally binding contract, it is not as complicated and long as another contract. It is not written in deep legalese, so you can understand and execute it without any legal knowledge. Here is the process involved in preparing this document:

Step 1: Identify the Terms

The borrower and lender must begin by identifying the terms of the agreement and agreeing to them verbally. The topics to cover include:

- The loan amount

- The applicable interest rate, otherwise called the fee for borrowing. You should check the interest rate laws (usury rate) in your country when setting this.

- Any late payment penalties

- Repayment terms, e.g., lump sum, installments, or incrementally

- A default clause explaining what happens if the borrower fails to repay the loan.

- The security or an item or property provided by the borrower to stand in if they fail to repay the amount.

- A co-signer or party that can be held financially liable if the borrower defaults.

Step 2: Conduct a Credit Check

Next, the lender must get legal permission to run a credit check on the borrower and learn if they have any outstanding debts. Debts related to child support or the IRS will usually take precedence over the loan given through a promissory note, so it is important to know.

Step 3: Identify the Security and Co-Signer

If the credit check-raises some concerns, the lender can request that the borrower gets a co-signer that will assume the debt if the former defaults. The borrower may also elect to put up security, e.g., a vehicle, valuable asset, or real estate (through a mortgage).

Step 4: Prepare the Promissory Note

When the lender and borrower agree on all the terms, they can prepare the promissory note – which we discuss below. They can then exchange the money after signing the letter.

Note: A witness is not a requirement but is highly recommended. You should also consider getting a notary public if the lending amount exceeds $10,000.

Step 5: Settle the Loan

Lastly, the borrower must ensure they pay back the loan per the payment terms set in the note. Once they make the full payment, the lender must release them from liability by issuing them a Loan Release Form. Late payments can be addressed through a Demand Letter and defaults by filing a claim through Small Claims Court or assuming ownership of the security.

Promise to Pay Letter (Promissory Note) Templates

How to Write a (Promissory Note) Promise to Pay Letter

As previously mentioned, you don’t need legal knowledge to understand or create a promissory note. The following guide will help you draft an effective Promise to Pay Letter:

Step 1: Identify the Lender and Borrower

Start by indicating the date (day, month, and year) when the promissory note is prepared. Identify the borrower and lender by their full names and personal or company addresses. Then, let the lender indicate the principal loan amount in words and numbers and the applicable interest rates.

Step 2: Highlight the Payments

Next, describe how the borrower is expected to repay the amount, i.e., by installments or as a lump sum. If you choose the former, indicate the frequency and amount of the installments. Both terms should be accompanied by a late fee amount to cover late payments.

Step 3: Define the Security

Decide whether the agreement will be ‘Secure’ or ‘Unsecure.’ Pawn shops usually use the former, but the latter is more appropriate when lending to an individual or company because it implies a level of trust. If you choose ‘Unsecure,’ identify the security.

Step 4: Identify the Co-Signer

Record the full name of a co-signer who will ensure the lender is repaid if the borrower defaults.

Step 5: State the Governing Law

Indicate the state where the exchange is happening and whose laws will govern the agreement.

Step 6: Sign the Note

Lastly, have the lender, borrower, co-signer, and possibly a witness sign the note.

How to Calculate

When creating a promissory note, several amounts are quoted, and it is crucial that you know how to calculate them. These include total interest, monthly payments, and total payout, and the following formulas will help you:

Total Interest Owed

Total Interest Owed = Money Borrowed × Annual Interest Rate

If the payments are made monthly or quarterly, you should divide the answer you get by the fraction of the year in which you will repay the amount. For example, if you borrow $10,000 for 6 months at an interest rate of 5%, the total interest for a year would be:

$10,000 × 5% = $500

The total interest owed is then arrived at by dividing this amount by 2 (because there are 2 6-month periods in a year) to get $250 as the total interest owed.

Final Payment Amount

Final Payment Amount = Money Borrowed + Total Interest Owed

Now, the total money you will owe at the end of the 6 months will be:

$10,000 + $250 = $10,250

Monthly Payment Amount

Monthly Payments = Final Payment Amount ÷ Number of Months

Lastly, since you have 6 months to repay the loan, your monthly payment will be:

$10,250 ÷ 6 = $1,708.33

Key Terms and Clauses

Here are some common key clauses and terms you will come across in a promissory note:

- Attorney’s Fees and Costs – These are the costs arising from court proceedings to handle a borrower defaulting the loan. The borrower usually pays them unless they prevail in court.

- Allocation of Payments – This describes how the borrower must make payments regarding the principal loan amount, interest, and late fees.

- Acceleration – This clause allows the lender to demand immediate payment for all the outstanding amounts if the borrower fails to meet the set payment timeline.

- Waiver of Presentments – A short clause stating that the lender need not demand payment because the borrower is responsible for making payments within the allotted time.

- Prepayment – A clause covering the rules for early payments.

- Non-Waiver – A clause confirming that the lender does not waive their rights if they fail or delay to exercise them per the agreement terms.

- Execution – Identifies the borrower as the Principal in the note and liable for all payments. Can also identify the borrower and co-signer as equally responsible.

- Severability – States that the voidance or unenforceability of one clause does not deem the entire note or other provisions invalid.

- Integration – Confirms that no other document can affect the validity or terms of the note.

- Conflicting Terms – Confirms that no other agreements have control or superior legality over the promissory note.

- Notice – Outlines how the lender must deliver a notice to the borrower. Standard practice is either by certified mail or in person.

- Co-Signer – The party guaranteeing the loan should the borrower default.

Frequently Asked Questions

Who signs a promissory note?

A promissory note must at least be signed by the borrower, although the lender could also sign it. If the amount being borrowed is significant, it is also important to get a witness and notary’s signature.

What happens if you don’t sign a promissory note?

An unsigned promissory note is void and legally unenforceable. The same can be said for a previously signed note in which changes were made without the lender or borrower’s approval.

What happens if you break a promissory note?

A promissory note is a legally binding contract, and defaulting or breaching it could lead to the loss of your security or other legal actions.

Do promissory notes expire?

Yes. Promissory notes have a statute of limitations ranging from 3 to 15 years, depending on the state. Once this timeline expires, they cannot be enforced in a court of law.

Is a handwritten promissory note a legal document?

Yes, a promissory note is a legally binding agreement, whether handwritten or typed, as long as it is signed. However, handwriting this document is not recommended as it can easily be altered.

Conclusion

A promise to pay letter is a legally binding agreement that indicates that a borrower will repay a sum of money lent to them by a private lender. It is important to know that altering the letter or including inaccurate information could null and void the contract. Essentially, you have to be very detailed and attentive when preparing this document of you will lose the ability to enforce it legally.